Dynamic Financial Stress Indicators Using Machine Learning: An Adaptive Composite Framework for Early Warning and Systemic Risk Assessment

DOI:

https://doi.org/10.59543/zrej1n55Keywords:

Composite stress indicator, Machine learning, Financial market stress, Early warning systems, Gradient boostingAbstract

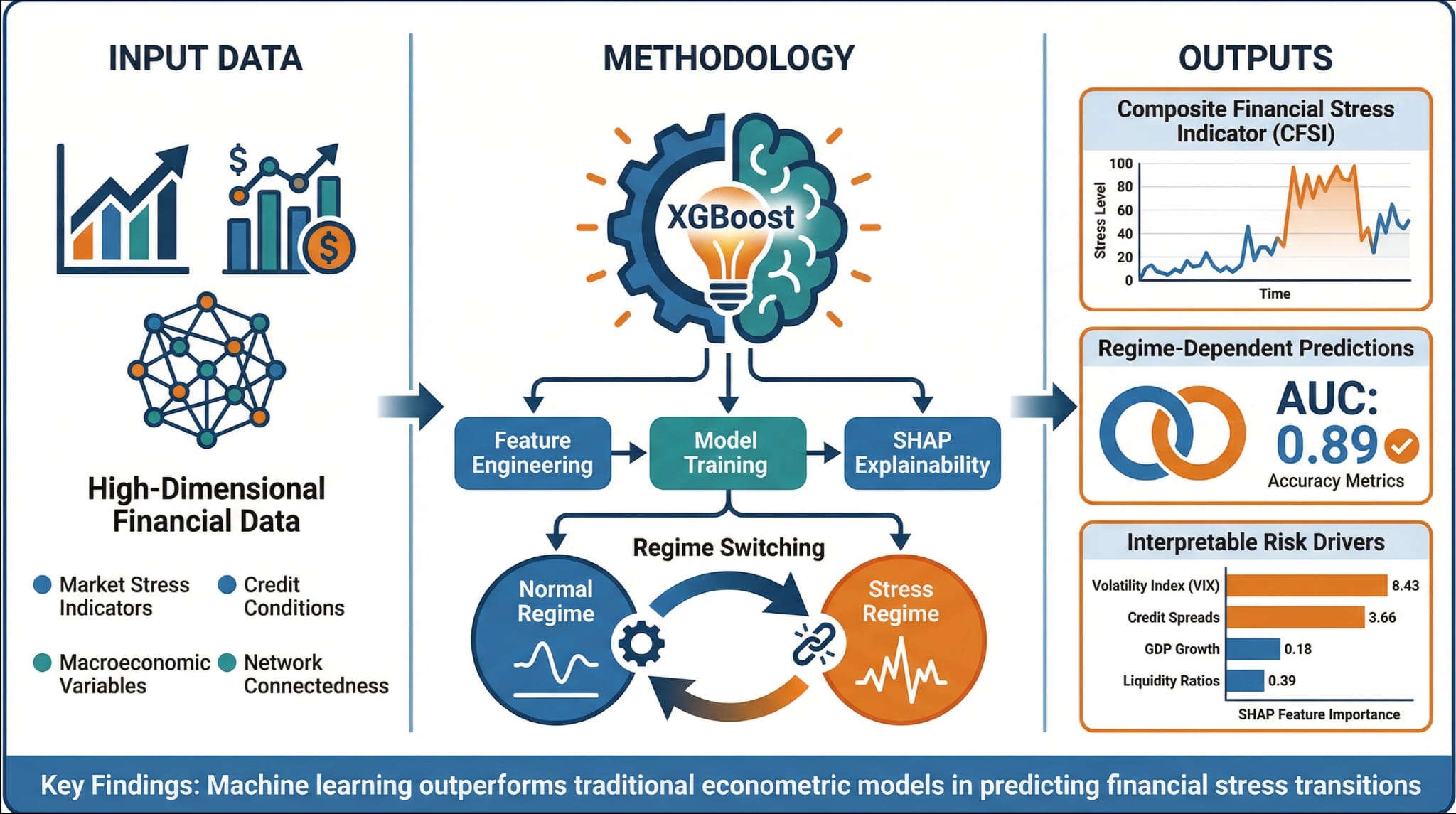

The present study proposes a machine learning-enhanced forecasting framework for financial stress that addresses critical limitations in static threshold approaches used by regulatory authorities. Utilizing a comprehensive dataset comprising daily S&P 500 information spanning multiple crisis episodes, we employ gradient boosting algorithms with dynamic threshold detection to predict market stress occurrences. The hybrid ensemble model utilized in this study has been shown to significantly surpass conventional econometric methods in terms of forecasting accuracy and the timeliness of early warning systems. The framework demonstrated a high degree of efficacy in predicting major crisis events during the hold-out period, exhibiting a substantial improvement in detection rates when compared to Federal Reserve indices. The application of feature importance analysis has yielded findings that demonstrate the presence of regime-dependent patterns. These findings indicate that there is a notable increase in sensitivity to real-economy variables, such as unemployment, during periods of recession. For practitioners, the continuous stress probability forecasts enable graduated risk management protocols and generate tangible portfolio gains. Researchers are particularly interested in the establishment of novel benchmarks for financial stress forecasting and in how machine learning can capture non-linear transmission mechanisms that conventional approaches cannot detect.

Downloads

Published

How to Cite

Data Availability Statement

The authors are willing to provide detailed documentation of data sources, variable definitions, and construction methodologies upon reasonable request to facilitate replication. All data preprocessing scripts, feature engineering code, model training procedures, and analytical scripts implementing the XGBoost, Random Forest, and LSTM architectures are available from the corresponding author upon request, subject to appropriate data use agreements and acknowledgment of intellectual property rights.

Issue

Section

License

Copyright (c) 2026 Abdullah Kürşat Merter, Yavuz Selim Balcıoğlu (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.

ABSJ is published Open Access under a Creative Commons CC-BY 4.0 license. Authors retain full copyright, with the first publication right granted to the journal.